Standard ACH Processing for Business: A Guide

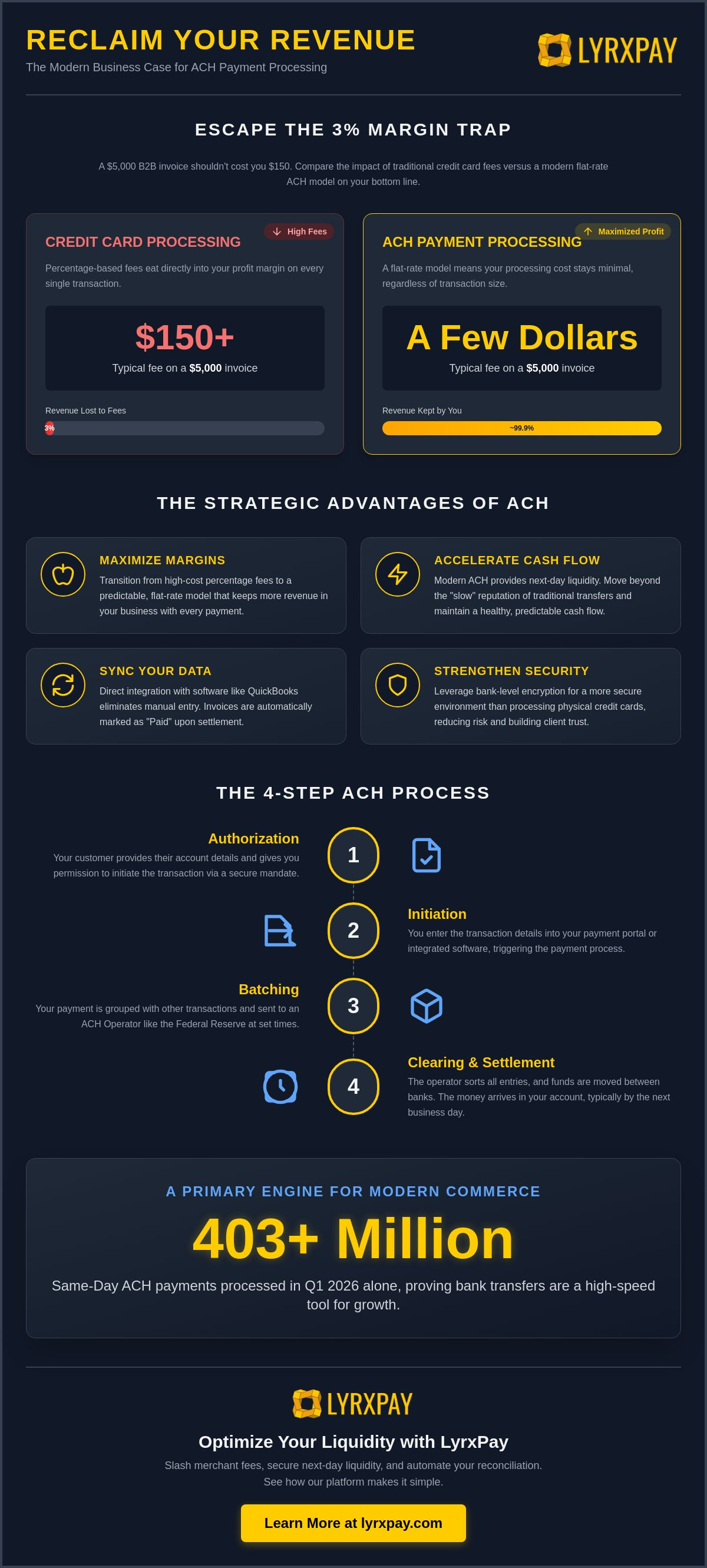

How much of your hard-earned margin is currently being sacrificed to 3% credit card processing fees just to ensure your cash stays liquid? It's a frustrating reality for many business owners who feel trapped between high transaction costs and the need for fast settlement. You shouldn't have to choose between keeping your profits and maintaining a healthy cash flow. Modern ach payment processing has evolved into a strategic backbone for B2B liquidity. It's no longer a slow alternative; it's a high-speed tool for growth. In fact, the Same-Day ACH network processed over 403 million payments in the first quarter of 2026 alone, proving that bank transfers are now a primary engine for modern commerce.

We know that manual data entry and slow settlement times can stall your momentum. This guide will show you how to slash those merchant fees and secure predictable, next-day liquidity. You'll learn how to automate reconciliation with QuickBooks and navigate the new June 2026 Nacha fraud monitoring rules with ease. We've done the heavy lifting to simplify these complex shifts. Now, we're presenting you with the most efficient path forward to optimize your operational health and reclaim your revenue.

Key Takeaways

- MAXIMIZE MARGINS. Discover how to transition from high-cost percentage fees to a flat-rate model that keeps more revenue in your business.

- ACCELERATE CASH FLOW. Learn how modern ach payment processing provides next-day liquidity, moving beyond the "slow" reputation of traditional bank transfers.

- SYNC YOUR DATA. See how direct integration with software like QuickBooks eliminates manual entry by automatically marking invoices as "Paid" upon settlement.

- STRENGTHEN SECURITY. Gain peace of mind by leveraging bank-level encryption that offers a more secure environment than processing physical credit cards.

UNDERSTANDING ACH PAYMENT PROCESSING: The Strategic Low-Fee Alternative

Why should a credit card network get a percentage of your success? It's a question more business owners are asking as they look to protect their bottom line. Understanding the mechanics of modern finance is the first step toward reclaiming your margins. What is an Automated Clearing House (ACH)? Managed by Nacha, this network serves as the electronic plumbing for the U.S. financial system, moving funds directly between bank accounts without the need for expensive card networks or slow paper checks.

The primary appeal for modern businesses is the radical difference in fee structures. While credit cards charge a percentage of every transaction, ach payment processing generally relies on a flat-fee model. Think about a $5,000 B2B invoice. A credit card processor might take $150 or more in fees. With ACH, that same transaction costs a tiny fraction of that amount, regardless of the total value. By 2026, savvy companies are making ACH their default for high-ticket items because every percentage point saved is a point added directly to their liquidity.

We view this shift as a form of advocacy for your business. You've done the hard work; you should keep the profit. By shifting away from the percentage-based trap of traditional card processing, you're not just cutting costs. You're building a more resilient financial foundation where your growth isn't taxed by the very tools you use to collect payment. It's about transparency and ensuring your resources go toward your craft rather than administrative overhead.

ACH Direct Debit vs. Direct Deposit

It's helpful to distinguish between the two ways money moves through this network. Direct Debit is the tool for your receivables, allowing you to pull funds from a customer’s account once they've provided a mandate. This is ideal for fixed-rate subscriptions or recurring service contracts. Direct Deposit, however, is for your payables, such as payroll or vendor payments. In short, "pull" transactions bring money into your business, while "push" transactions send money out to others.

Why Transaction Volume Matters

Scalability is where ACH truly shines. As your transaction volume increases, the savings compared to credit cards become impossible to ignore. Beyond the math, there's a level of professional trust involved. Many clients prefer the bank-level encryption of an ACH transfer over the risks associated with handling and storing physical card data. This transition is a key reason how ACH payments streamline business transactions for growing firms. It replaces the anxiety of high fees and data breaches with a steady, secure, and cost-effective workflow that supports long-term professional relationships.

HOW ACH TRANSFERS WORK: Timelines, Settlement, and Same-Day Options

How does money actually move from a client's bank account into yours without a physical card present? While the process happens behind the scenes, understanding the mechanics of ach payment processing helps you manage your cash flow with greater precision. It's not a single, instantaneous event like a credit card "swipe." Instead, it's a structured sequence of secure handshakes between financial institutions. According to Nacha's guide to ACH payments, this reliability is exactly why the network remains the preferred choice for massive B2B volumes.

The journey of an ACH transfer follows four distinct steps:

- Step 1: Authorization. Before you can pull funds, you must obtain a mandate from your customer. This is a legal agreement where they provide their routing and account numbers and give you permission to initiate the transaction.

- Step 2: Initiation. Once you have the green light, you enter the transaction details into your merchant portal or integrated accounting software. This tells the system exactly how much to move and when.

- Step 3: Batching. Unlike real-time systems, ACH transactions are grouped together into batches. Your payment processor sends these batches to an ACH operator, such as the Federal Reserve, at specific times throughout the day.

- Step 4: Clearing and Settlement. The ACH operator sorts the entries and sends them to the respective banks. Funds are then moved between the Originating Depository Financial Institution (ODFI) and the Receiving Depository Financial Institution (RDFI).

The Evolution of Speed: Same-Day ACH in 2026

Speed used to be the primary complaint regarding bank transfers. That has changed. In 2026, Same-Day ACH is a powerful tool for businesses that need to move money quickly. Currently, there's a $1 million per-transaction limit, which accommodates almost all standard business operations. To hit the same-day window, you must submit your batch by specific deadlines set by the network. If you miss the cutoff, the transaction simply moves to the next available window, ensuring your money is never sitting idle for long.

Standard vs. Fast Settlement

Standard processing typically takes between one and three business days. The exact timing often depends on how quickly your ODFI processes the batch and the specific risk policies of your processor. While three days might seem long in a digital world, it provides a layer of security and verification that protects against fraud. Reliable settlement speed is the primary factor in maintaining consistent business liquidity and operational confidence. If you're looking to bridge the gap between low fees and high speed, you might consider how modern processing solutions can provide the next-day deposits your business requires to stay agile.

ACH VS. CREDIT CARDS VS. WIRE TRANSFERS: A Decision Framework

Choosing the right payment rail isn't just about technical preference; it's a strategic financial decision that impacts your daily liquidity. While we've explored the mechanics of ach payment processing, you need to know how it stacks up against the alternatives to make an informed choice. Credit cards offer speed but at a steep percentage cost. Wire transfers provide immediate finality but come with hefty fixed fees. ACH sits in the "sweet spot" for most B2B operations, offering a balance of security and affordability that others simply can't match.

Security is a major differentiator here. ACH uses bank-level encryption, which means you aren't storing sensitive 16-digit card numbers that could be compromised in a data breach. There's also the matter of reversibility. The rules for reversing an ACH transaction are much stricter than credit card chargebacks. A customer can't dispute an ACH payment simply because they changed their mind; they generally need to prove the transaction was unauthorized or the amount was incorrect. This provides a layer of protection for your revenue that credit cards often lack.

To help you decide, consider this quick framework for your next invoice:

- Use ACH for: High-ticket B2B invoices, recurring subscriptions, and payroll where cost-efficiency is the priority.

- Use Credit Cards for: Small, one-off retail transactions or when the customer insists on using their rewards points.

- Use Wires for: Immediate, multi-million dollar transactions that require instant settlement, such as real estate closings.

The "Hidden Cost" of Credit Cards

Most business owners see the headline rate and think that's the end of the story. It isn't. Interchange fees and processor markups can turn a simple transaction into a complex web of deductions that are difficult to track. For high-ticket industries like legal services, medical practices, or wholesale distribution, these percentage "taxes" eat directly into your scaling potential. If you're ready to audit your statements and reclaim your profit, check out our guide on how to lower merchant fees to see exactly where your money is going.

Wires: The High-Speed, High-Cost Alternative

Wires are the "emergency room" of payments. They're necessary when minutes matter, but they are expensive and "push-only," meaning the sender must initiate every single payment. This makes them a poor choice for recurring billing. ACH is the superior choice for long-term B2B relationships because it allows for "pull" flexibility and costs significantly less. Why pay for a wire's speed when Same-Day ACH can often achieve the same goal for a tiny fraction of the price? By choosing the right tool for the job, you demonstrate a level of managed care for your business's financial health.

STREAMLINING OPERATIONS: Integrating ACH with QuickBooks and Xero

Is your bookkeeping team spending hours every week manually matching bank deposits to open invoices? This administrative drag is more than just a nuisance; it's a drain on your operational health. When you integrate ach payment processing directly with your accounting software, you transform your back office from a bottleneck into a streamlined engine. Instead of "chasing checks" or typing in routing numbers, you're creating a system where the data flows automatically from the transaction to the ledger.

The real magic happens through automated reconciliation. When a customer pays via an integrated link, your software recognizes the payment and automatically marks the invoice as "Paid" in real time. This eliminates the risk of human error that often leads to double-billing or missed payments. We believe in providing a "concierge" level of service, which means having a partner who understands how your QuickBooks or Xero setup functions. It's about more than just moving money; it's about managed care for your entire financial workflow, ensuring your books are always accurate without the midnight stress.

QuickBooks Integrated Payment Processing

Whether you use QuickBooks Online, Pro, or Premier, the benefits of integration are immediate. By leveraging all in one business financial solutions, you can embed a "Pay Now" link directly into your digital invoices. If the customer clicks that link, they can securely authorize an ACH transfer in seconds. This triggers a seamless data sync that updates your books without a single keystroke from your staff. We've already done the heavy lifting to ensure your payment portal and your accounting software speak the same language, allowing you to focus on your craft rather than data entry.

Automating Recurring B2B Invoices

For long-term clients, "set it and forget it" billing is the ultimate goal. You can establish recurring ACH pulls that occur on a specific date every month, ensuring you get paid without having to send a single reminder. This consistency is a cornerstone of effective business liquidity management. When you know exactly when your receivables will hit your account, you can plan your next growth phase with total confidence. If you're ready to stop the manual data entry and start scaling, explore our integrated ACH solutions today to see how we can simplify your operations and protect your time.

OPTIMIZING YOUR LIQUIDITY: The LyrxPay Advantage for ACH

Why settle for a vendor when you can have a defender of your resources? Most providers treat ach payment processing as a utility, a cold transaction that happens in the background. We take a different approach. By focusing on lower-fee structures for the national market, we act as an advocate for your margins. We've seen how high fees can stifle a company's ability to reinvest. Our mission is to remove those obstacles, providing the professional confidence you need to manage your business's health without the stress of hidden costs.

LyrxPay positions itself as a long-term ally. We don't just process your payments; we understand how those payments impact your bookkeeping and overall financial narrative. Because we specialize in both processing and accounting support, we bridge the gap between your bank account and your ledger. This proactive stance allows you to focus on your craft while we handle the administrative heavy lifting. It's a concierge style of service that anticipates your needs before they become obstacles.

Next-Day Deposits and Improved Cash Flow

Standard timelines often leave business owners waiting three to five days for their funds to settle. In a fast-paced environment, that delay is unacceptable. We've accelerated the traditional timeline to offer next-day deposits, ensuring your cash is available when you need to meet payroll or purchase inventory. This commitment to merchant liquidity is a core pillar of our service. If your money isn't moving as fast as your business, your growth is being artificially capped. Faster settlement means you can respond to market opportunities with agility and maintain a healthy, predictable cash flow.

B2B Payment Processing Solutions for Growth

Whether you're running a boutique firm or a national fleet, your infrastructure must be scalable. We provide customized solutions for professional services and medical offices where financial health is paramount. Our systems are designed to grow with you, from your first hire to your hundredth. You deserve a partner who anticipates your needs and offers curated service for your unique operational workflow. We pride ourselves on making the complicated feel manageable, allowing you to scale with integrity and clarity.

Streamline your ACH processing with LyrxPay today.

RECLAIM YOUR REVENUE AND SIMPLIFY YOUR WORKFLOW

Transitioning to a modern ach payment processing strategy is one of the most effective ways to protect your margins and optimize your business liquidity. You've seen how moving away from percentage-based credit card fees can immediately boost your bottom line. By integrating these payments directly into your QuickBooks or Xero environment, you aren't just saving money; you're buying back your time. No more manual reconciliation or midnight bookkeeping sessions; just a clean, automated flow of data that keeps your records accurate.

We understand that managing the administrative side of a business can be overwhelming. That's why we focus on providing a "managed care" experience that goes beyond simple transactions. With our next-day deposits and expert accounting integration, you can stop chasing checks and start focusing on your true craft. We bring a national reach with a personal, Texas-based concierge touch to every partnership, ensuring you always have an ally in your corner.

Ready to see the difference? Switch to LyrxPay for Lower ACH Fees and Next-Day Deposits and take control of your financial future. You've built a great business; let's ensure your payment systems are strong enough to support your next big leap.

Frequently Asked Questions

What is the difference between ACH and a wire transfer?

ACH is a batch-processed, bank-to-bank transfer managed by Nacha, while a wire transfer is a real-time, individual transaction. ACH is significantly cheaper and allows for "pull" transactions where you collect from customers. Wires are "push-only" and carry high fixed fees. While wires offer immediate finality for multi-million dollar real estate deals, ACH is the superior choice for scalable, recurring B2B billing.

How long does an ACH payment take to process in 2026?

Standard processing typically takes one to three business days, but the network has become much faster. If you submit your transactions before the daily network cut-off times, Same-Day ACH allows for settlement within the same business day. We focus on providing next-day deposits to ensure your cash stays liquid, bridging the gap between traditional bank timelines and your immediate operational needs.

Is ACH payment processing safe for my business and customers?

Yes, ach payment processing is highly secure because it relies on bank-level encryption and direct financial communication. You don't have to store sensitive 16-digit card numbers, which significantly reduces your risk in the event of a data breach. Strict Nacha rules also protect your business from unauthorized entries, providing a level of managed care and security that physical checks simply can't match.

Can I integrate ACH payments with QuickBooks or Xero?

You can absolutely integrate your bank transfers with leading accounting software to eliminate manual data entry. Integrated systems automatically sync your transaction data, marking invoices as "Paid" the moment funds are verified. This creates a seamless workflow where your bookkeeping stays current without the need for manual reconciliation. It's a proactive way to reduce human error and keep your financial records accurate.

What are the typical fees for ACH payment processing?

ACH typically uses a flat-fee model rather than the percentage-based fees common with credit card processing. This means you pay a consistent amount per transaction regardless of the total invoice value. It's often the most cost-effective choice for high-ticket B2B transactions. By avoiding the 3% "tax" of card networks, you keep more of your hard-earned revenue and improve your overall business margins.

Is there a limit on how much I can send via ACH?

The current per-transaction limit for Same-Day ACH is $1 million, as established by the governing body, Nacha. While standard ACH may allow for larger amounts depending on your specific merchant account and risk profile, this $1 million cap covers almost all daily business operations. If your business requires moving larger sums, we can help you navigate the necessary authorizations to keep your money moving.

How do I set up an ACH merchant account?

Setting up an account involves providing your business credentials, bank details, and estimated transaction volumes to a processor like LyrxPay. We guide you through the underwriting process to ensure your account is configured for your specific industry needs. Once approved, you can start initiating "pull" debits from customers or "push" deposits to vendors and employees through a secure, professional portal.

What is Same Day ACH and how do I use it?

Same Day ACH is a feature that allows for faster clearing and settlement within the same business day. To use it, you flag your transactions for same-day processing and submit them before the daily network deadlines. It's an excellent tool for urgent payroll or emergency vendor payments. This flexibility allows you to respond to market opportunities with agility while maintaining a predictable and healthy cash flow.