Mobile Credit Card Processing for Business: The 2026 Buyer’s Guide

What if your payment setup actually helped you keep more of your revenue instead of just taking a cut? For most owners, mobile credit card processing for business feels like a necessary evil, often defined by high fees that eat into margins and hardware that fails right when a customer is ready to pay. You're likely tired of finishing a long day of sales only to spend another hour manually entering data into QuickBooks while waiting days for your funds to arrive. It's a frustrating cycle that makes you feel like you're working for your processor rather than the other way around.

You deserve a partner that acts as a defender of your time and resources. This guide reveals how to choose a solution that lowers your merchant fees, secures your data, and automates your back-office workflows. We'll break down the impact of the 2026 Credit Card Competition Act, explain how to leverage the latest interchange rate reductions, and show you how to achieve next-day deposits with hardware that actually works. It's time to move past the flat-rate traps and find a professional-grade workflow that treats your business like the priority it is.

Key Takeaways

- Learn how to transition from basic card readers to a cloud-synced ecosystem that supports professional-grade hardware and modern Tap to Pay technology.

- Identify hidden markups in flat-rate pricing. Discover why interchange-plus models offer the most transparent way to lower your processing costs.

- Select a mobile credit card processing for business solution with built-in offline capabilities to maintain reliable sales even in remote locations.

- Recover lost hours by implementing native integrations with QuickBooks or Xero to automate your daily bookkeeping and eliminate manual entry.

- Understand the benefits of a concierge approach to merchant services that prioritizes your profit margins through dedicated advocacy and managed care.

Evaluating Mobile Credit Card Processing for Business in 2026

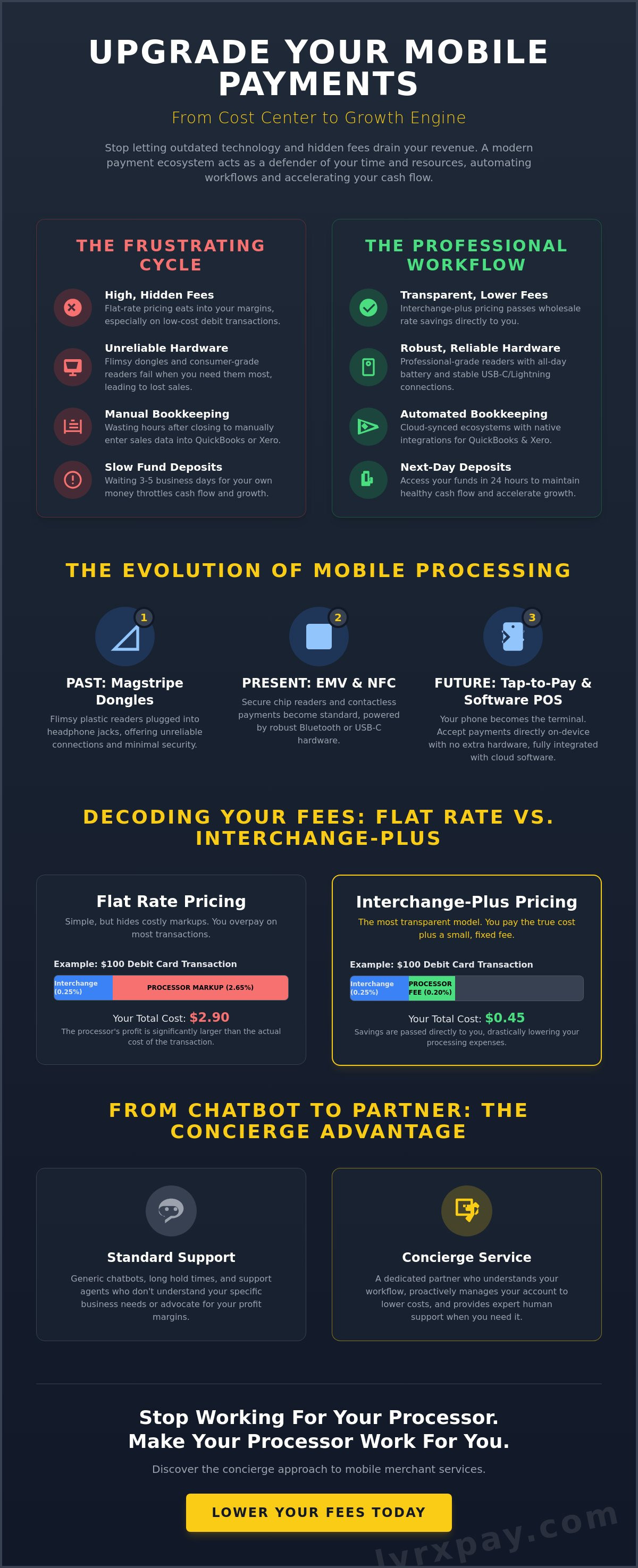

Mobile processing used to be a compromise. You'd plug a flimsy plastic dongle into a headphone jack and hope the connection held long enough to swipe a card. In 2026, that version of mobile credit card processing for business is obsolete. Modern systems are no longer just peripherals; they're fully integrated, cloud-synced ecosystems. This shift means that a payment taken on a smartphone in the field is instantly reflected in your back-office bookkeeping and inventory. Speed and software integration are now the baseline, not the exception.

The transition from magnetic stripes to Mobile payment systems using NFC (Near Field Communication) and EMV chip technology has redefined security. We've moved beyond the swipe. Today, "Tap to Pay" on mobile devices allows you to accept payments directly on a smartphone without any extra hardware at all. For professional services like law firms or medical practices, this removes the "front desk" friction that often delays collections. When the payment process is invisible, the focus stays on the service provided.

The Evolution of the Mobile Merchant

Reliability has reached a tipping point. Thanks to 5G connectivity and advanced encryption standards, mobile processing is now arguably safer than traditional landline terminals. We're seeing the rise of "software-only" POS solutions where the device in your pocket becomes a secure terminal. Because the technology is more complex, business owners are moving away from DIY big-brand apps. They're choosing "concierge" support models where they can actually speak to a human who understands their specific workflow. If your hardware fails or a deposit is delayed, you need a partner, not a chatbot. It's about moving from a transaction to a relationship.

Who Benefits Most from Mobile-First Payments?

While retail uses these tools for "line-busting" to keep customers happy, other sectors are seeing even greater gains. Field service professionals, such as HVAC technicians and plumbers, now rely on mobile credit card processing for business to secure on-site settlement before leaving a job site. This eliminates the "check is in the mail" excuse and drastically improves cash flow. Professional offices are also adopting these tools to allow patients or clients to pay discreetly from an exam room or consultation office. It's about meeting the client where they are, rather than forcing them into a rigid administrative process. If you can settle an invoice in thirty seconds on a tablet, you've removed the biggest hurdle to getting paid.

Core Features of High-Performance Mobile Payment Solutions

High-performance mobile credit card processing for business requires more than just a sleek app or a low-profile reader. It demands hardware that survives the physical demands of daily field use. While consumer-grade "dongles" are often cheap or even free, they frequently fail at the most inconvenient times, leading to lost sales and frustrated clients. Professional-grade readers offer superior battery life and physical resilience, ensuring you can process transactions all day without a recharge. If your hardware feels like a toy, it's likely treating your revenue like one too.

Beyond the physical device, your solution must provide robust offline processing. If you lose signal in a remote service area or a concrete-shielded basement, you shouldn't lose the sale. High-performance systems securely store encrypted data and process it the moment you're back online. This reliability is the difference between a successful on-site settlement and a "we'll bill you later" scenario that creates an administrative headache. Financial velocity is equally critical. Waiting three to five business days for your funds to clear is an outdated practice that throttles your cash flow. In 2026, next-day deposits are the standard for healthy operations. You can find more about optimizing your financial flow by looking into modern merchant services that prioritize your business margins.

Hardware vs. Software: Finding the Balance

Reliability often comes down to how your reader communicates with your device. While Bluetooth offers convenience for many, Lightning or USB-C connections provide a more stable link for high-volume environments where interference is common. The software interface must be intuitive enough that staff training takes minutes, not hours. Speed in the field is essential, but it can't come at the cost of safety. PCI-DSS compliance serves as the mandatory security baseline that ensures every mobile transaction is handled within a strictly regulated and secure environment.

Security Protocols You Must Demand

Protecting your customers is a non-negotiable part of your professional reputation. Tokenization is the gold standard; it replaces sensitive card data with a unique identifier, ensuring that even if your system is compromised, the actual card details remain safe. This significantly reduces your liability and aligns with cybersecurity best practices provided by the SBA. Additionally, EMV chip technology is your primary defense against fraudulent chargebacks. For a deeper look at protecting your revenue and data, read the ultimate reference to secure credit card processing solutions in 2026. These layers of protection allow you to focus on your craft while your processing system acts as a silent defender of your resources.

Comparing Fee Structures: Flat-Rate vs. Lower-Fee Merchant Services

Transparency is the foundation of a healthy partnership. Many providers push flat-rate pricing because it sounds simple. A fee like 2.6% plus 10 cents per transaction is easy to calculate, but it often hides a 40% markup on the actual costs of processing. This is the "Flat-Rate Trap." For established companies, this simplicity is actually a convenience tax that drains your margins. When you use mobile credit card processing for business, you shouldn't be penalized for your success as your volume grows.

We believe in a different approach. Interchange-plus pricing is the most transparent model available because it separates the actual cost charged by the card brands from the processor's markup. This ensures you know exactly where every penny goes. Beyond the base rates, you must also audit your statements for hidden "gotchas." Statement fees, PCI non-compliance penalties, and gateway surcharges can quietly add hundreds of dollars to your monthly bill. At LyrxPay, our mission is to act as a defender of your resources by focusing on lower-fee solutions that protect your bottom line.

Understanding the Real Cost of a Swipe

Every transaction consists of three parts: interchange fees set by the banks, assessment fees from card brands like Visa or Mastercard, and the processor markup. If you want to maximize your profit, "wholesale" rates should be your goal. These rates pass the raw costs directly to you with a small, fixed margin on top. To see how these components affect your specific industry, you can review our guide on how to lower merchant fees. Understanding this breakdown is the first step toward reclaiming your revenue.

The Impact of Volume on Your Choice

The right choice depends on your monthly sales volume. Flat-rate pricing usually makes sense for micro-businesses processing under $3,000 per month because the fixed costs of other models might outweigh the savings. However, once you cross that threshold, the break-even point shifts dramatically. For businesses scaling past $10,000 a month, switching to interchange-plus can save thousands of dollars annually. It's also vital to prioritize avoiding common mistakes like ignoring deposit delays. Next-day deposits improve business liquidity and operational agility by putting your funds to work immediately.

Streamlining Operations: Integration with QuickBooks and Xero

Most buyers focus entirely on the front-end transaction, but the real efficiency gains happen in your back office. Manual bookkeeping is a hidden cost that drains hours of your time every single week. If your mobile credit card processing for business doesn't talk to your accounting software, you are essentially working two jobs. You are a business owner during the day and an unpaid data entry clerk at night. This manual gap is where errors happen, leading to mismatched deposits and hours of frustration during tax season.

The solution lies in native, direct integration. While some providers rely on third-party "bridges" or apps to connect their systems, these tools often break or create messy duplicate entries. A high-performance mobile solution uses a direct sync to automate the creation of sales receipts, the calculation of sales tax, and the reconciliation of merchant fees. This isn't just about saving time; it's about accuracy. When your processing and accounting live in the same ecosystem, your financial forecasting becomes a reliable tool rather than a best guess. If you are ready to stop the manual entry cycle, explore our QuickBooks integrated merchant services to automate your workflow today.

Eliminating the "Data Entry Gap"

Modern mobile payments can automatically populate QuickBooks or Xero in real-time. This means that the moment a client taps their card in the field, the invoice is marked as paid and the funds are tracked for reconciliation. This process significantly reduces human error when matching mobile sales with your actual bank deposits. For a step-by-step look at how to sync your systems, read our QuickBooks bookkeeping services for small business guide. This level of managed care for your administrative tasks allows you to focus on your craft while the software handles the numbers.

Inventory and Sales Reporting on the Go

A connected mobile system does more than just move money. It acts as a mobile command center for your operations. You can use mobile POS data to track stock levels across multiple locations or service vehicles in real-time. For professional services like medical or legal offices, reporting can be customized to track specific billable events or client categories. Generating "End of Day" reports directly from your mobile device gives you instant clarity on your daily performance without needing to open a laptop. It's about having the pulse of your business in the palm of your hand.

LyrxPay: The Concierge Approach to Mobile Merchant Services

Most providers view your account as a line item on a spreadsheet. At LyrxPay, we treat mobile credit card processing for business as a partnership that requires ongoing advocacy. We don't just set you up and disappear into a self-service portal. We act as a defender of your margins by constantly looking for ways to lower your fees and remove operational friction. While big-box processors leave you to figure out frozen accounts or hidden fee spikes on your own, our concierge model ensures you always have a professional ally in your corner.

Cash flow is the lifeblood of your operations, which is why we've moved past the industry standard of multi-day delays. Next-day deposits ensure your liquidity matches the pace of your sales, allowing you to reinvest in your business immediately. We also handle the heavy lifting of technical setup. Our team manages the integration with QuickBooks and Xero so your back office is automated from day one. You focus on your craft; we'll manage the administrative health of your business.

Beyond the Card Reader

Our service extends far beyond just moving money. We offer a comprehensive suite of solutions including Payroll, Bookkeeping, and advanced Point of Sale hardware and software. Based in Texas with a national reach across all 50 states, we provide the localized attention of a boutique firm with the scale required to support growing enterprises. This is why professional offices, from medical practices to legal firms, choose LyrxPay to manage their merchant services. We understand that your time is your most valuable asset, and we aim to protect it by consolidating your essential workflows into one reliable ecosystem.

Ready to Lower Your Processing Costs?

Switching to a more efficient system shouldn't be stressful. We've refined our transition process to be seamless and straightforward. It begins with a free statement audit where we identify the hidden fees and markups currently eating into your profits. We provide a clear, transparent comparison so you can see exactly how much you'll save by moving to a lower-fee model. There are no high-pressure tactics, just honest data and a path toward better financial health. If you're ready to stop overpaying for convenience, contact LyrxPay for a customized mobile processing quote to start your audit today.

RECLAIM YOUR MARGINS AND YOUR TIME

The landscape of mobile credit card processing for business has shifted from a simple convenience to a strategic financial workflow. Moving away from the "flat-rate trap" and embracing transparent pricing stops you from overpaying for every swipe. Integrating your payments with QuickBooks or Xero isn't just a luxury; it's a necessity for any professional looking to eliminate the burden of manual bookkeeping and data entry errors.

You shouldn't have to wait days for your revenue or spend your evenings reconciling receipts. LyrxPay provides a concierge approach that includes a lower-fee guarantee compared to flat-rate processors, next-day deposits for all merchants, and seamless software integration. We've done the heavy lifting so you can focus on growing your business with total confidence. Get a Free Merchant Fee Audit from LyrxPay and start keeping more of what you earn today. Your business health is our priority, and the most efficient path forward is just a conversation away.

Frequently Asked Questions

Is mobile credit card processing safe for my business?

Modern mobile processing is highly secure because it utilizes end-to-end encryption (E2EE) and tokenization. These technologies ensure that sensitive card data never actually touches your device. Instead, a unique token represents the transaction, which significantly reduces your liability and protects your customers from data breaches. As long as you use PCI-compliant hardware and software, your mobile transactions are just as safe as traditional terminal payments.

How much does mobile credit card processing actually cost?

The total cost depends on whether you choose a flat-rate or an interchange-plus pricing model. While flat rates are simple to understand, they often include a high markup that eats into your margins. Interchange-plus is more transparent, passing the raw cost of the card brand fee directly to you with a small, fixed margin on top. Auditing your monthly statement is the best way to uncover hidden surcharges and non-compliance fees that inflate your costs.

Can I take mobile payments without a card reader?

Yes, you can accept payments using "Tap to Pay" technology on compatible smartphones or by manually keying in card details through a virtual terminal. While keyed-in transactions usually carry higher fees due to increased risk, Tap to Pay uses the same secure NFC technology as a physical reader. This allows for a professional checkout experience without the need for extra hardware when you're working in the field.

How long does it take to get my money from mobile sales?

High-performance solutions now offer next-day deposits to keep your cash flow moving at the same pace as your sales. While some older or consumer-grade processors still take three to five business days to clear funds, modern mobile credit card processing for business prioritizes liquidity. Getting your funds quickly allows you to pay vendors, manage payroll, and reinvest in your operations without unnecessary waiting periods.

Will mobile processing work with my existing QuickBooks software?

Professional-grade mobile solutions offer native integration with QuickBooks and Xero to automate your back-office tasks. This allows your sales data to sync automatically, which eliminates the need for manual data entry and late-night bookkeeping. Choosing a system with direct sync for mobile credit card processing for business ensures that your sales receipts, taxes, and merchant fees are always reconciled accurately without duplicate entries.

What happens if I lose my internet connection while taking a payment?

Reliable mobile systems include offline processing capabilities that allow you to capture encrypted transaction data even without a signal. The system securely stores the information and processes the payment automatically once your device reconnects to a network. This feature is essential for field service professionals who often work in remote areas, parking garages, or basements where cellular reception is unreliable.

Do I need a separate merchant account for mobile processing?

In most cases, your mobile processing will be tied to a single merchant account that handles all your transaction types. A concierge-style provider will help you set up an account that covers mobile, in-office, and online payments under one unified system. This consolidation makes it much easier to track your total volume and negotiate better rates as your business grows, rather than managing multiple fragmented accounts.

How do I avoid high chargeback fees with mobile payments?

The most effective way to prevent chargebacks is to use EMV chip readers for every in-person transaction. Chip technology provides a higher level of authentication than magnetic stripes, which helps protect you from "fraudulent use" claims. Additionally, sending digital receipts immediately and using a clear "doing business as" name on bank statements helps customers recognize their purchases and reduces accidental disputes.