B2B Payment Processing Solutions: The 2026 Guide to Streamlined Operations

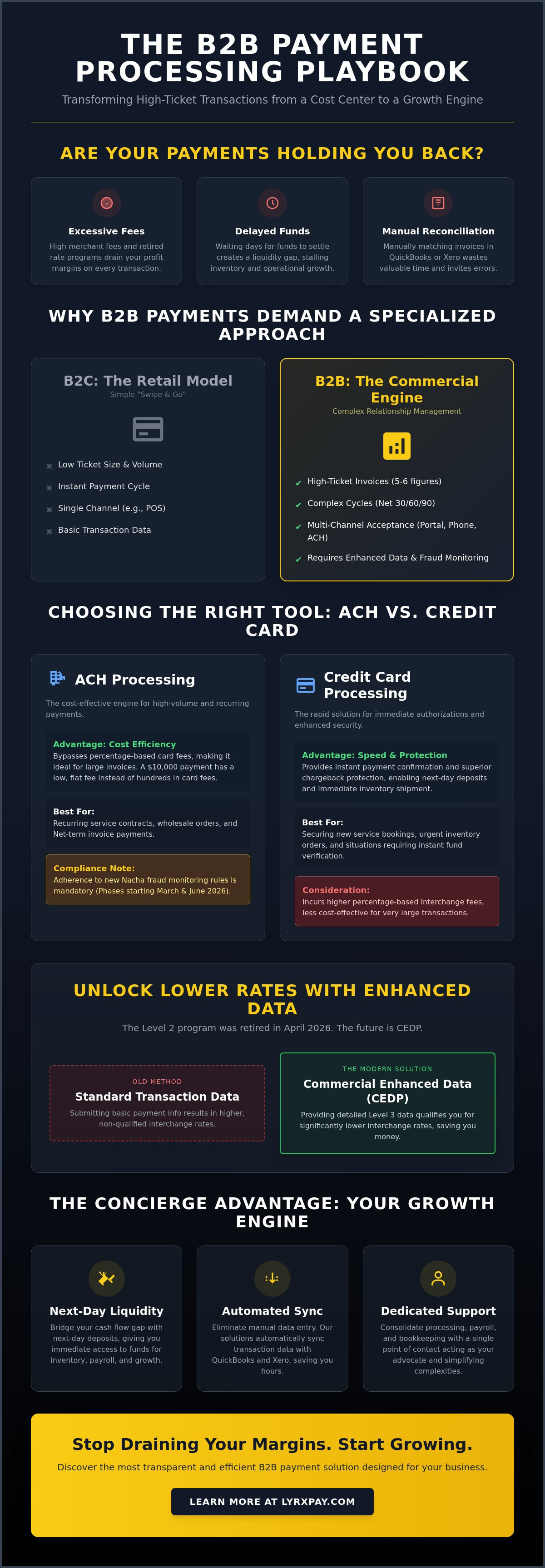

Why are you still paying premium rates for Level 2 data when the program was officially retired in April 2026? It's a frustrating reality for many leaders who realize their current B2B payment processing solutions are draining their margins instead of supporting them. You likely know the stress of watching high merchant fees chip away at your profits while you wait days for funds to settle. It's even more taxing when you have to spend your evenings manually matching invoices in QuickBooks or Xero because your gateway won't talk to your ledger.

We're here to act as your advocate and simplify these complexities. This guide will help you master the nuances of modern transactions to unlock next-day liquidity and transparent, lower-fee structures. You'll learn how to navigate the shift to the Commercial Enhanced Data Program (CEDP) and implement automated syncs that handle the heavy lifting for you. We'll explore the latest ACH fraud monitoring rules and the exact steps to turn your payment processing from a manual chore into a streamlined engine for growth.

Key Takeaways

- Understand why high-ticket B2B transactions require specialized infrastructure and multi-channel acceptance to handle net-term invoicing effectively.

- Learn to balance the cost-efficiency of ACH processing for recurring billing against the speed and convenience of credit card authorizations.

- Identify hidden service fees and discover why interchange-plus pricing is the most transparent model for scaling your B2B payment processing solutions.

- Discover how next-day deposits can bridge your liquidity gap, giving you immediate access to funds for inventory and operational growth.

- Explore the "concierge" advantage of consolidating your processing, payroll, and bookkeeping through a single, dedicated point of contact.

Why B2B Payment Processing Solutions Differ from B2C Systems

Think about the last time you bought a coffee. You swiped, the transaction was approved in seconds, and the interaction ended. In the world of wholesale distribution or medical offices, that simplicity is a myth. B2B payment processing solutions must account for a landscape where a single invoice might equal a retail store's entire weekly revenue. You aren't just moving money; you're managing a complex relationship defined by contracts and credit terms.

If your business relies on Net-30 or milestone-based billing, a standard retail gateway will likely fail you. These systems aren't designed to track a payment that happens weeks after the service is rendered. They also struggle with multi-channel needs. A wholesaler might need to accept a digital payment through a portal, take a credit card over the phone, and process an ACH transfer for a recurring shipment. This requires a foundation in sophisticated e-commerce payment systems that can bridge the gap between digital and physical touchpoints without losing track of the ledger.

Transaction Volume and Ticket Size

High-value transactions carry a different weight of responsibility. When a transaction reaches five or six figures, the risk profile shifts. Specialized fraud monitoring becomes essential to protect your cash flow from chargebacks that could cripple your monthly margins. Beyond security, the data you send with a transaction matters. With Visa officially retiring the Level 2 interchange program in April 2026, businesses must now utilize the Commercial Enhanced Data Program (CEDP). By providing Product 3 data, you can access lower rates that retail-focused processors simply can't offer. It's a proactive way to defend your resources.

Complexity of the Payment Cycle

The "swipe and go" mentality doesn't work when you're managing Net-60 terms or complex service-based milestones. Traditional B2C gateways often lack the reporting depth needed for multi-stakeholder approval processes. Your accounting team needs to know exactly which invoice a partial payment belongs to without spending hours on manual reconciliation. Effective B2B payment processing solutions act as a bridge. They move the transaction data directly into your financial workflow, ensuring that when a client pays, your bookkeeping is updated instantly. This eliminates the friction between your sales department and your back office, allowing you to focus on your craft rather than administrative cleanup.

Core Mechanisms: ACH vs. Credit Card Processing for Business

Choosing between ACH and credit cards isn't a binary decision; it's a strategic move to optimize your cash flow. While one prioritizes cost, the other prioritizes speed. Understanding how these mechanisms work within modern B2B payment processing solutions allows you to defend your margins while keeping your clients happy. This alignment is a core part of ongoing B2B payments modernization efforts, which aim to replace slow, manual checks with efficient electronic flows that provide better data and faster resolution.

The Power of ACH for High-Volume B2B

If you're managing recurring service contracts or wholesale orders, ACH is your most reliable ally. ACH processing stands as the most cost-effective method for high-ticket B2B invoices. By moving funds directly from one bank account to another, you bypass the percentage-based fees that make card networks expensive for large sums. Integrating this directly into your digital invoicing means your clients can pay with a few clicks, creating a seamless experience that mirrors retail convenience without the retail price tag. It's also vital to stay compliant with the 2026 Nacha fraud monitoring rules. Phase 1 began on March 20, 2026, for large originators, and Phase 2 starts June 19, 2026, for all remaining non-consumer originators. These rules ensure that while your costs stay low, your security remains ironclad.

Credit Card Processing: Speed and Protection

There are moments when immediate authorization is worth the higher fee. If you need to ship inventory today or secure a high-value service booking, credit cards provide the instant confirmation ACH sometimes lacks. This method offers superior chargeback protection and simplifies the access to Next-Day Deposits, which is vital for maintaining a healthy cash flow. By using a dedicated merchant account, you can handle large card transactions with confidence, knowing the funds are verified instantly. If you're looking for a partner who can help you navigate these choices without hidden markups, exploring transparent merchant services can provide the clarity your business deserves.

Ultimately, a hybrid approach is often the most resilient path. By offering both methods, you empower your clients to choose what fits their internal procurement rules while you maintain control over your settlement times. Whether you're prioritizing the low overhead of ACH or the rapid liquidity of card processing, the goal is the same: removing every obstacle between you and your revenue. Protecting sensitive business banking data is no longer just a technical requirement; it's a foundational part of the trust you build with your professional partners.

Evaluating the Real Cost of B2B Transactions

Do you actually know what you're paying for every dollar processed? Most business owners look at the headline percentage and assume they've done their due diligence. However, the true cost of B2B payment processing solutions often hides in the fine print of a monthly statement. It's not just about the transaction rate. It's about the monthly service charges, gateway fees, and the "junk fees" that provide zero value to your operations. We believe in total transparency because you can't defend your margins if you don't know where the leaks are occurring.

Interchange-plus pricing remains the most honest model for a growing company. This structure passes the direct "wholesale" cost from the card networks straight to you, with a clearly defined, fixed markup from your processor. Unlike tiered or flat-rate models, it doesn't hide extra profit in "non-qualified" surcharges. If you want to optimize your bottom line, understanding this breakdown is non-negotiable. It allows you to see exactly what Visa or Mastercard charges versus what your service provider keeps for their support.

Decoding Your Merchant Statement

Statements are often intentionally dense. They're designed to make you glance at the total and move on. You might find "PCI non-compliance fees" even if you're compliant, or "statement fees" for a digital document. These are often avoidable costs that eat into your profits. Learning how to lower merchant fees starts with a professional fee audit. By identifying these markups, you can reclaim resources that are better spent on your inventory or team. We take pride in making the complicated feel manageable by highlighting these discrepancies for our partners.

The ROI of Integrated Financial Solutions

Think about the "hidden tax" of manual data entry. If your payment gateway doesn't talk to your ledger, you're paying a staff member or a bookkeeper to do the heavy lifting of reconciliation. That's a real cost. When you choose B2B payment processing solutions that integrate directly with your payroll and bookkeeping, you're not just buying a service; you're buying back time. An all-in-one financial partner reduces administrative overhead by ensuring that a payment received in the morning is reflected in your QuickBooks or Xero account by the afternoon. This level of managed care allows you to focus on growth rather than chasing down missing transaction records.

Maximizing Liquidity with Next-Day Deposits and Integrated Workflows

Have you ever checked your processing dashboard to see a massive wholesale order marked as "pending," only to realize those funds won't hit your bank for nearly a week? This is the liquidity gap. In the world of business-to-business commerce, waiting 3 to 5 days for funds to clear is more than a minor annoyance; it's a bottleneck that prevents you from restocking inventory or meeting payroll obligations. Modern B2B payment processing solutions should do more than just authorize a transaction. They must act as an accelerator for your capital, ensuring that your revenue is ready to be reinvested the moment it's earned.

Solving the Cash Flow Crunch

Next-Day Deposits improve business liquidity by ensuring that today's sales are available in your operating account by tomorrow morning. If you can access your revenue within 24 hours, you can settle your own vendor obligations without relying on expensive short-term credit lines. This speed also helps you proactively reduce your Days Sales Outstanding (DSO). When you pair rapid settlement with automated payment reminders, you create a self-sustaining cycle of cash flow. There is a profound sense of relief that comes from seeing your hard-earned revenue reflected in your balance sheet almost immediately, allowing you to focus on growth rather than survival.

Seamless Accounting Integration

Accounting shouldn't be a separate, manual chore that follows your sales process. The true "Holy Grail" of B2B payment processing solutions is a direct, automated sync with software like QuickBooks or Xero. By eliminating manual data entry, you remove the risk of human error and reclaim hours of administrative time every single week. This integration ensures that your financial forecasting is based on real-time data rather than week-old spreadsheets. If your ledger updates the moment a payment is settled, you always have an accurate pulse on your business health. You can maintain strict PCI compliance while offering a fast, integrated checkout experience that feels professional to your clients and effortless for your team.

Ready to bridge the liquidity gap and get your funds faster? Switch to next-day deposits today and reclaim control over your business cash flow with a partner who understands your operational needs.

LyrxPay: A Concierge Approach to B2B Merchant Services

Most large-scale processors treat business owners like a number in a database, prioritizing transaction volume over personal partnership. We take the opposite approach. At LyrxPay, we act as a defender of your resources by focusing on transparent, low-margin B2B payment processing solutions that actually serve your bottom line. Whether you are managing a medical office, a professional service firm, or a retail wholesale operation, your needs go beyond a simple "swipe." You need a partner who understands that every dollar saved on merchant fees is a dollar that can be reinvested into your team, your inventory, or your brand presentation; to see how custom branding can support your professional image, learn more about The CEO Creative and their selection of office essentials.

The transition to a more efficient financial model shouldn't be a source of stress. We've built our business on the idea of managed care for your administrative tasks. By providing a single point of contact for your processing, payroll, and bookkeeping, we eliminate the need for you to juggle multiple vendors. This integrated approach ensures that your data flows smoothly from the point of sale directly into your financial records, giving you the clarity you need to lead with confidence.

Beyond Standard Processing

We don't stop at just authorizing transactions. Our expertise in QuickBooks integration means we do the heavy lifting of ensuring your payment gateway and your accounting software are in perfect sync. When you pair our merchant processing with our professional bookkeeping services, you remove the burden of manual reconciliation entirely. Our Texas-based team provides a concierge level of service that larger, impersonal firms simply lack. If you have a question about a settlement or need to update your payroll configuration, you talk to a real person who knows your business, not a generic call center.

Your Path to Lower Fees and Faster Funding

Moving forward is easy. The first step toward optimizing your B2B payment processing solutions is a straightforward audit of your current merchant statement. We'll help you identify the hidden markups and junk fees that are eating into your margins. During your first 30 days with LyrxPay, we focus on setting up your integrated workflows and ensuring your next-day deposits are flowing correctly. We are here to prove that financial services can be supportive, honest, and deeply invested in your success.

Ready to see the difference that a dedicated financial ally can make for your operations? Discover how LyrxPay can lower your B2B processing fees today and start reclaiming the time and money your business deserves.

RECLAIM YOUR OPERATIONAL FREEDOM

Your revenue should be an engine for growth rather than a source of administrative stress. We've explored how the right B2B payment processing solutions can bridge the liquidity gap and replace manual data entry with seamless automation. By prioritizing next-day deposits and expert QuickBooks or Xero integration, you aren't just moving money. You're building a more resilient, efficient business that's ready to scale.

Are you tired of wondering where your margins are disappearing? It's time to stop settling for hidden fees and slow settlement times. You deserve a partner who acts as a defender of your time and resources. Whether it's through lower-fee ACH processing or a curated merchant account, the goal is to make the complicated feel manageable. If you have the right infrastructure in place, then you can finally shift your focus from the ledger back to your clients.

Start your free merchant statement audit with LyrxPay today to uncover hidden costs and unlock faster funding. We're ready to do the heavy lifting so you can focus on your craft. You've built a great business; let's make sure your financial infrastructure is just as strong.

Frequently Asked Questions

What is the most cost-effective B2B payment processing solution?

ACH processing is generally the most cost-effective method for business transactions because it uses low flat fees or small percentage caps instead of the high rates found on card networks. For large wholesale orders, switching to ACH can save your business thousands in overhead costs every year. It's a straightforward way to defend your margins without changing your core sales process.

How long does it take for B2B payments to hit my bank account?

While standard settlement can take several days, modern B2B payment processing solutions provide Next-Day Deposits. This means funds from today's sales are available in your operating account by tomorrow morning. If your business relies on rapid inventory turnover or tight payroll cycles, this speed is essential for maintaining healthy liquidity and avoiding the need for short-term credit.

Can I integrate my B2B payment processor with QuickBooks?

Direct integration with QuickBooks and Xero is a standard feature for professional-grade processors. This link allows your payments to sync automatically with your accounting software the moment they settle. It removes the stress of manual reconciliation and ensures your financial forecasting is always based on the most current data available, allowing you to focus on growth instead of administrative cleanup.

Is ACH processing safer than credit card processing for large transactions?

Both methods are secure, but they offer different types of protection for your revenue. Credit cards provide instant authorization and chargeback rights, while ACH uses the Nacha network's 2026 fraud monitoring rules to secure bank-to-bank transfers. Your processor should use high-level tokenization to ensure that sensitive banking data never touches your local servers, keeping your professional relationships protected.

What are Level 2 and Level 3 processing data, and why do they matter for B2B?

These data levels refer to the amount of detail sent with a transaction, such as tax IDs and line-item descriptions. Following the retirement of Visa's Level 2 program in April 2026, businesses should focus on providing Product 3 data under the Commercial Enhanced Data Program (CEDP). This extra information proves the transaction is a legitimate business expense, which triggers lower interchange rates from the card brands.

How do I switch B2B payment processors without disrupting my current billing?

Switching doesn't have to be a headache if you have a partner to manage the data migration. Your new provider should help you move your stored client profiles and recurring billing schedules securely. By running the new system in parallel with your old one for a few days, you can ensure a seamless handoff that doesn't affect your clients' experience or your cash flow.

Are there hidden fees in most B2B payment processing contracts?

Many traditional contracts hide markups in "non-qualified" rates or monthly service fees that add no value. A transparent model for B2B payment processing solutions will use interchange-plus pricing, which separates the card network's cost from the processor's markup. We always suggest a professional audit to identify and remove unnecessary "junk fees" from your monthly statements to reclaim your profits.

What is the difference between a payment gateway and a merchant account?

Think of the payment gateway as the digital terminal that captures the payment and the merchant account as the holding tank for your funds. The gateway validates the transaction data, while the merchant account ensures you actually receive the money after it's processed. You need both working in harmony to transform a client's "pay" click into a usable bank deposit.